Product Overview

DiscoverPrint’s Personalised Receipt Book is a versatile and practical solution designed to meet your specific record-keeping requirements. Whether you’re a small business owner, freelancer, or simply need a personalised system for tracking expenses, our receipt books offer a customised touch to your documentation process.

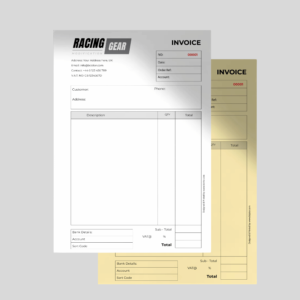

With the ability to add personal or business details, such as logos and names, these receipt books are tailored to reflect your unique identity. The professional appearance not only adds a touch of sophistication but also streamlines the organisation of your financial transactions. Whether you’re issuing receipts for sales, services, or any other transactions, our Personalised Receipt Book provides a convenient and personalised way to keep track of your financial records.

By choosing DiscoverPrint for your Personalised Receipt Book, you’re opting for a solution that combines functionality with personalisation, making the process of recording transactions efficient and reflective of your individual or business style. Stay organised and make a lasting impression with our customisable receipt books.

Use For: to keep track of transactions and give customers confirmation of purchase.

1 review for Personalised Receipt Book

There are no reviews yet.